Working paper · SLAM

Seeing Like a Market

The rationale for institutional risk transfer using prediction markets: a 90-page working paper and 87 contracts across five asset classes.

Quick initial links

Our research has four outputs:

- A summary of the working paper at www.slampaper.xyz

- An exploration tool for examining that pipeline at https://www.slampaper.xyz/explorer

- A working paper (truly still WIP)

- A desk-quality data pipeline (accessible on the site)

Two Forms of Order

Prediction markets have been, primarily, studied as forms of speculation and as truth machines. Both forms of framing are correct and extremely analytically useful.

In the case of the former, most volume is still primarily retail driven, and one can argue that the prima materia of any form of financial innovation has been by primarily two things. First, the desire to speculate and win. Secondly, to create more efficient forms of financing. A keystone example here being the rise of the Amsterdam Stock Exchange and bond issuance as a way to finance the Dutch War of Independence against the Hapsburgs (it worked). The latter cannot exist without the former, so it holds.

The second already explores a new frontier. Crowd sourced epistemology. That frame has generated the entire intellectual infrastructure of the category. Valid. Extremely important. However, the theory for this frame has already been set and has been well-explored, with most empirical studies just substantiating and proving initial priors.

Is there another way to understand prediction markets? We believe you can. You can think about them structurally. The structural question is different. Not what prediction markets know, but what they are. Are they a completely new form of market structure, or are they an information layer that sits on top of existing market exposures and asset classes providing informative flow?

This is why we wrote Seeing Like a Market. It is an early working paper that seeks to understand prediction markets as a structural object, and, through that, whether prediction markets can, in theory, act as a far superior form of hedging and coverage for actors that want large notional exposures through the elimination of the path costs that are part and parcel of buying binary options for discrete events off a traditional desk.

First, a direct cost comparison between prediction markets and derivatives for pricing the same binary risk at institutional scale. Second, that prediction markets are but a purer form of binary options, an alternative market topology for contingent claims. For the first two, we construct a theoretical framework to analyze that difference.

Third, that the intellectual framework used by many people, including Chris Dixon justifying the Kalshi round last year, which was rooted in Hayek's 1945 essay on price signals, is correct but incomplete. Hayek wrote a second framework. Applying it to market microstructure changes the analysis.

The Bet

A friend of mine spent close to twenty years in FICC, studied under Scholes at Chicago Booth etc. He has a feel for how derivative pricing works at the institutional level. The version where someone warehouses risk overnight and explains the P&L in the morning.

When I told him prediction markets could displace options for pricing binary institutional risk, he said it wouldn't work. In fact, he told me that I am wasting my time and it's stupid. As any rational human being would do when confronted with twenty years of experience versus just my solid intuition, I ended up building a theoretical measurement framework, a cost-comparison analysis, which ended up being a ninety page working paper trying to construct a new frame on how to think about prediction markets structurally (with empirical validation)

The results were clear. His skepticism was mitigated and he was brought on as a reviewer. When the work started, nobody was talking about institutional adoption of event swaps or prediction markets. Right now, it's one of the key central narratives in the entire category. We did not expect this to happen so fast.

Thank you

I wanted to extend my thanks to the @Kalshi and the @KalshiResearch team for inviting me to the Kalshi Research conference and giving me the chance to explain some of the core arguments on the frontier research panel, as well as providing some initial feedback on the work.

Moreover, I wanted to thank some of my friends for actually going through a 90 page working paper and providing initial feedback. I am shocked and grateful.

Two Forms of Order

Everyone cites Hayek's 1945 paper, "The Use of Knowledge in Society." Prices aggregate dispersed knowledge. The telecommunications system of the economy. This is what grounds the informational thesis: prediction markets produce better forecasts than polls or expert panels because they aggregate private beliefs into a price. It's crowd-sourced epistemology.

Hayek wrote a second framework. In Law, Legislation and Liberty (1973), he drew a distinction between two forms of order. Taxis: constructed order, designed and maintained deliberately. Cosmos: spontaneous order, emerging from participants following rules without anyone coordinating the result. He applied it to legal systems and social institutions. My previous research as a grad student at the London School of Economics applied that latter piece to the CDS market to understand systemic contagion during the GFC. The same framework is applicable here.

The volatility surface is Taxis. Dealers build it. They run models, warehouse inventory, manage risk, post capital, comply with regulation. The surface is a machine that produces prices for contingent claims. It works. And it charges for its own maintenance.

A "pure" prediction market order book is Cosmos. No bilateral dealers outside of block trades. The models are probabilistic and are true to ground-tooth, and not a form of volatility pricing that imposes a certain frame on the market. Dispersed participants post prices based on private views. The market matches them. The price is the result of participation, not apparatus.

Both can price binary risk. One charges for the infrastructure. One doesn't. The cost differential is not a market inefficiency waiting to be arbitraged. It's structural, a direct consequence of the distinction between constructed and emergent order.

The paper calls the total gap the Vega Wedge. Three components. The variance risk premium: markets charge for volatility uncertainty even when the outcome is discrete, so the institution pays for path risk it doesn't carry. Dealer balance sheet: Basel III made maintaining the pricing machine more expensive, and clients rent it whether they need intermediation or not. Replication friction: constructing a binary payoff from continuous instruments requires multiple legs, each introducing spread and slippage.

On FOMC contracts, the Wedge runs around 0.7%. Sounds small. Across the institutional flow that hedges discrete monetary policy risk globally, it is not small. And FOMC is the cheap case, where the apparatus is most efficient because the underlying is most liquid. For contested elections, for emerging market central bank decisions, the Wedge widens to 2–4%.

Prediction markets price the same binary directly. One contract. One price. Pricing pure probability.

This does not mean that HFTs or MMs aren't actively helping make markets on prediction market exchanges. The argument is slightly more subtle than that. The argument is that even with large makers participating on markets, what can be called "toxic" or "bad" flow will still lead to statistically similar distributions relative to traditional derivatives markets (which are mostly all proxy in nature), where the volatility seller infrastructure is absolutely necessary to create these markets, but also to produce signal in an ocean of noise.

Why Institutions Are Coming In (And what we don't look at)

The research makes a displacement claim. Capital migrates when the embedded tax exceeds the switching friction. What's happening now is every layer of the institutional stack building around that migration.

I will not go on repeating verbatim the convergence that we're seeing right now when it comes to prediction markets and institutional adoption. You know it's getting serious when you see the event definitions of a CLN getting defined based on prediction market outcomes.

It's happening and our research creates a plausible theory (with empirical evidence) of why that displacement is happening. However, I want to make a few points clear about what the paper does not do:

- It's not a GE model for prediction markets, as that would require full operationalization of a margin model

- For the purposes of our research, we are deliberately excluding margin. It's important, but it will also get solved. At this point in time, we do not want to state a claim or a view on what kind of margin model will work best

- We don't say that prediction markets are going to displace all forms of derivatives trading. We are saying that it is highly likely they are most cost-effective for hedging when it comes discrete events. And, more importantly, that signal quality is not lost

What We Found

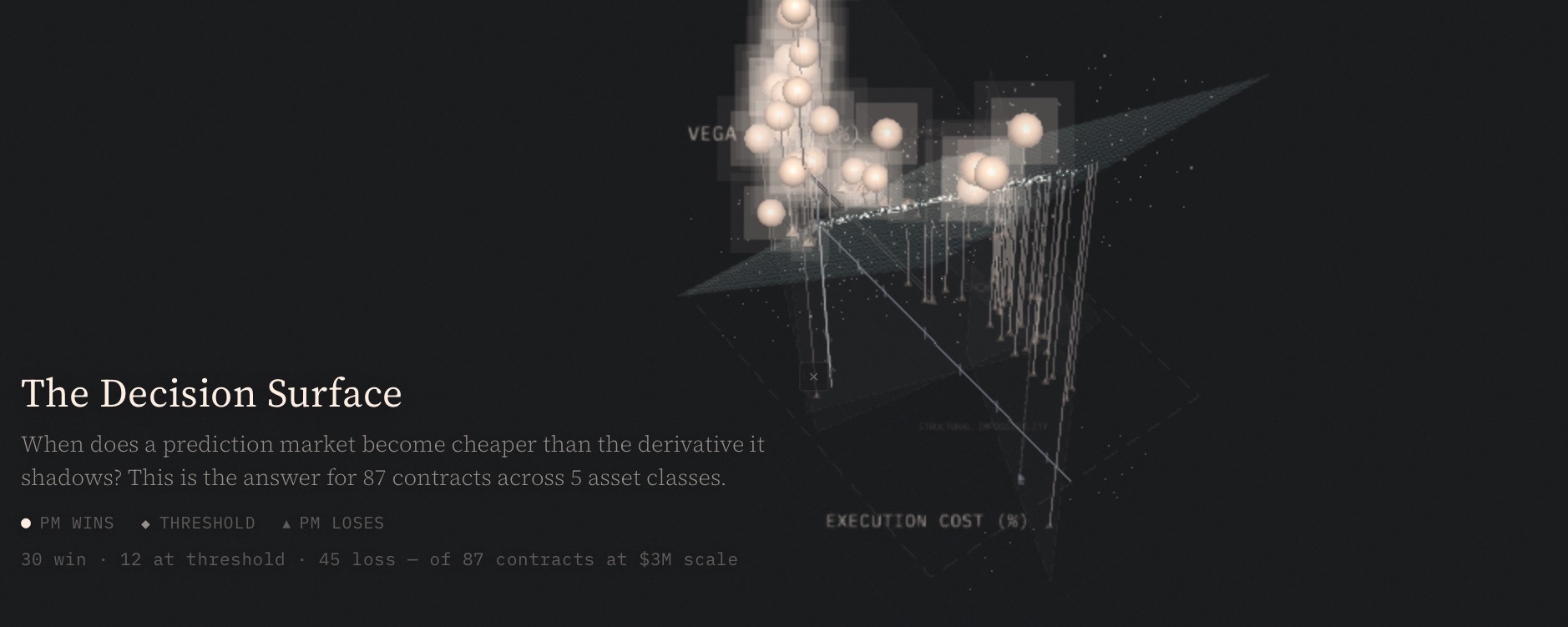

The paper predicts that categories where the Vega Wedge is widest, where the apparatus charges the most, flip first. Categories where the apparatus is efficient flip last. The VRP gradient orders the sequence.

BTC event contracts crossed twelve of twenty cost thresholds. Elections crossed twelve of seventeen. FOMC, the single most liquid binary event in the world, crossed zero of six. The predicted ordering held across the entire dataset.

The FOMC result is counterintuitive. You'd expect the deepest, most liquid markets to flip first. The opposite happened. The Fed Funds options infrastructure is so embedded in institutional plumbing (clearing, margining, regulatory reporting, two decades of desk workflow) that it's the most resilient to displacement. Constructed order persists where the maintenance costs are lowest relative to switching costs. The deepest apparatus survives longest, and that is what the framework predicts.

There's an additional dimension to the FOMC case that matters. To even measure what the options market charges for binary FOMC risk, the paper had to build a seven-step proxy decomposition. Fed Funds options — the natural derivative for hedging discrete rate decisions — are effectively unobservable. Databento returns zero rows. CME's own Liquidity Review omits them. CFTC weekly reports exclude them. Pit trading closed in May 2021. The observable market is unobservable.

One result isolates the mechanism cleanly. In January 2026, five BTC contracts shared identical VRP at 4.08% but had different strike prices and different volumes. Four of the five crossed the cost threshold. The one that didn't was the thinnest market. Same structural advantage, same underlying, same time period. The only variable that separated a PM win from a PM loss was liquidity depth. The Wedge was there in every case. Whether the prediction market could capture it depended on whether enough participants showed up.

The third finding extends beyond prediction markets. In derivatives, the volatility smile, the curvature of implied volatility across strike prices, is understood as a product of market microstructure. Dealer hedging flows. Inventory management. Institutional risk limits. Feedback between model recalibration and positioning. Billions of dollars of infrastructure producing a distributional signature.

We found the same signature in prediction market data. BTC touch-markets on Polymarket create a synthetic options chain from $75K to $125K strikes. We extracted implied volatility from 2.4 million trades. Fat tails. Skew. Regime dynamics.

This matters beyond the scope of this paper. The standard account in derivatives is that the smile is a product of volatility seller infrastructure: dealer hedging creates feedback loops between inventory, models, and positioning, and the resulting curvature encodes information about tail risk that wouldn't be visible otherwise. If that account is complete, you'd expect the smile to disappear when you remove the apparatus. It doesn't. The same curvature, the same information about how the market prices deviation from the expected outcome, shows up in a venue where none of that infrastructure exists.

Spontaneous order producing the same informational structure that constructed order charges to maintain. Hayek (1973), measured empirically in market microstructure.

How to explore?

I don't expect everyone to read a 90 page working paper. You can get the key arguments at www.slampaper.xyz. After that, you can visually explore the data set within the Explorer.

The paper and repo is accessible on the website. In the near future, we will make sure that the Explorer can handle external data sets, so that you can run your own CSVs or parquet files within the explorer to explore your own data sets, or make it comparable to our original one, or the datasets of other users. The intent is to be fully open source on this.

What the Framework Predicts

The framework predicts a sequence. High-VRP categories have already crossed. BTC and contested elections are cost-competitive at institutional scale today with the exclusion of margin. FOMC sits at threshold: nine of twelve contracts are within fractions of a percentage point of crossing, and execution costs compressed 78% over the sample period. The binding constraint there is spread, not depth, and spread compresses with market-maker competition. Low-VRP categories where the apparatus is efficient: liquid equity indices, silver, remain structurally unfavorable, and the framework predicts they should.

The framework also specifies what would break it. If prediction markets achieve sustained threshold crossing for a claim class and institutional flow does not migrate, if both forms of order persist at scale for the same function, the displacement prediction fails. If low-VRP categories cross before high-VRP categories, the gradient mechanism fails. Thirty contracts have crossed on cost. Whether flow follows is the next empirical question.