Market structure · benchmarks

Benchmarks are key to scaling prediction markets institutionally

Which benchmarks can actually do it, in what order — and why the benchmark slot is the one to own.

History does not repeat, but it does tend to rhyme. Alexander conquered the Known World, and so Caesar wept at his tomb in Alexandria, then went and built the same imperial form on different ground. Napoleon idolized Caesar, recodified Roman law into the Code Civil. Things recompose. Processes have path-dependencies and isomorphisms. Things that are shaped isomorphically tend to gravitate to the same solutions.

Institutional finance plays this rhyme particularly hard. Each new asset class runs through the same sequence of infrastructure layers as it transitions from retail-grade pricing to institutional-grade plumbing, because the operational requirements above any asset class are identical: methodology-grade references that institutional capital can mark against, audit, and report.

You see this rhyme being played in the institutional adoption of prediction markets right now. The same conversational threads as crypto in 2014–2016 and credit in 2002–2004. Have you read on CF Benchmarks? How did CDX and iTraxx come into being? How do you take a bunch of heterogeneous exposures and turn them into something homogeneous enough for institutional capital to touch.

That's the conversation a lot of people are having right now. Marex sold the first prediction-market-linked structured note: 10m notional, 7% coupon, hedged on Kalshi, sold to a Swiss client. Goldman's CPI event-linked note is moving through the pipeline. Roundhill's six prediction-market ETFs list Monday with Bitwise and GraniteShares filed behind. Bernstein is projecting 240bn in full-year 2026 prediction-market volume. Kalshi did $25.7bn in March alone.

Each of these in isolation is the kind of event that gets a Bloomberg writeup and rolls past. Taken together, in the past two quarters, they describe institutional capital arriving in a market that didn't have institutional capital twelve months ago. The question that occupied prediction-market discourse for the past two years (will institutions actually use these venues) is mostly closed. They are, or at least we're at the precipice of that being settled.

The more interesting question, and the one I actually want to write about, is where that capital lands first, and what it lands against. The instruments themselves go by various names: outcome markets, event contracts, binary options that strip out replication cost. The variable that decides where institutional flow lands is cost-efficiency relative to the alternatives institutional desks are already using to hedge the same risks.

The rhyme everyone's playing is the benchmark layer. CDX did it for credit, CF Benchmarks did it for crypto, and prediction markets are next. There's a real cluster of teams either fundraising or already deploying against this; I've had several inbound asks in the past month from investors looking to be connected with teams building benchmark and index methodology.

Operators like @0xperp have been writing about this publicly for a very long time. A tweet by @mittal_rahil went viral a few days ago when announced that he's looking into this as a builder. The ETF filers are positioning around an underlying that doesn't exist in standardized form yet. Some incumbent will walk the path S&P Global walked with Markit.

But the rhyme goes one step further than most of the people running the race are running it. The race-to-build is running upstream of the question tor whether any of this works: which benchmarks pull flow once they're live and which don't.

6 point tldr if you're short on time

Institutions cannot deploy against bilateral pricing. They need methodologies a regulated entity stands behind, computed at known cadence, auditable. Methodologies survive across screens and days; quotes don't. Everything downstream (marking, reporting, settling wrappers, hedging) is denominated in the reference.

The arithmetic has been done twice. Markit consolidated CDX and iTraxx, IPO'd at $4.5bn, sold inside IHS Markit to S&P. CF Benchmarks built BRR with under five people and $1.5m raised, captured 6 of 11 spot Bitcoin ETF NAVs, sold to Kraken for nine figures. Switching costs accumulate fast once wrappers settle, so the first family to earn adoption owns the reference for the next decade.

Why? You need benchmarks for anything that's a bit more sophisticated or structured beyond some of the more obvious financial instruments. A widely accepted benchmark becomes market standard and a part of the nomenclature.

The race-to-build is running upstream of the question of which benchmarks actually pull flow. Multiple teams are converging on the slot, but the slot only matters if the underlying contracts pass a cost test against the replication institutional desks already use. Methodology can be flawless and still pull zero AUM.

The cost test runs on two axes. Does a deliverable alternative exist, and how big is the VRP in that alternative. VRP (implied minus realized vol) is the academically-quantified price of the bundling problem. Options sell state and path coverage together; event contracts price terminal state alone. The wedge is the savings.

The structural wrinkle is the closing. In credit and crypto the underlying was deliverable, so the spot market matured for years and answered the cost test implicitly before any benchmark shipped. This cell has no spot to mature. So either the methodology shop runs the test upstream by measuring VRP in the closest replication, or allocators run it downstream on wrapper performance after the fact. Done right, this is one of the highest-margin businesses in finance for a novel asset class.

The benchmark slot

The reason this specific layer is the target, rather than any other piece of institutional infrastructure that capital arriving into prediction markets might need, is mechanical, and it's worth being precise about because it explains both why people are racing and why most of them will still get it wrong.

Institutional capital does not deploy against bilateral pricing. As a PM, you can't punt bets on Polymarket, Kalshi or any other prediction market exchange. Things are a little bit tougher. In general, you deploy against reference rates. By "reference rate" I mean a published methodology that some regulated entity stands behind, computed at a known cadence, available on every screen, that an auditor can sign off on and a custodian can verify.

The relevant property is that it's a methodology rather than a quote, and methodologies survive across screens and across days while quotes do not. The reason this matters is that everything an institutional allocator does downstream of holding the position requires that methodology-grade reference. Marking the book against it, reporting risk to regulators, settling wrappers, hedging the structured products built on top, computing fees and so forth.

This is foundational for building out a far more sophisticated array of instruments for this asset class. Bespoke structured needs benchmarks. Ask an old FICC banker on how fun it was to price a structured product for a municipality or sovereign without them having issued a USD-denominated bond before. It's not very fun without having a good benchmark when it comes to credit risk (do not confuse that with something like a CDX.)

Every prior asset class ran the same sequence. Spot liquidity reaches a threshold where pricing becomes consistent. A benchmark emerges with a published methodology that turns bilateral pricing into something replicable. Derivatives trade against the benchmark. Structured products and ETFs reference the derivatives. Each layer references the one below it, and the benchmark is the load-bearing slot. Everything downstream is denominated in it.

The credit and crypto comps

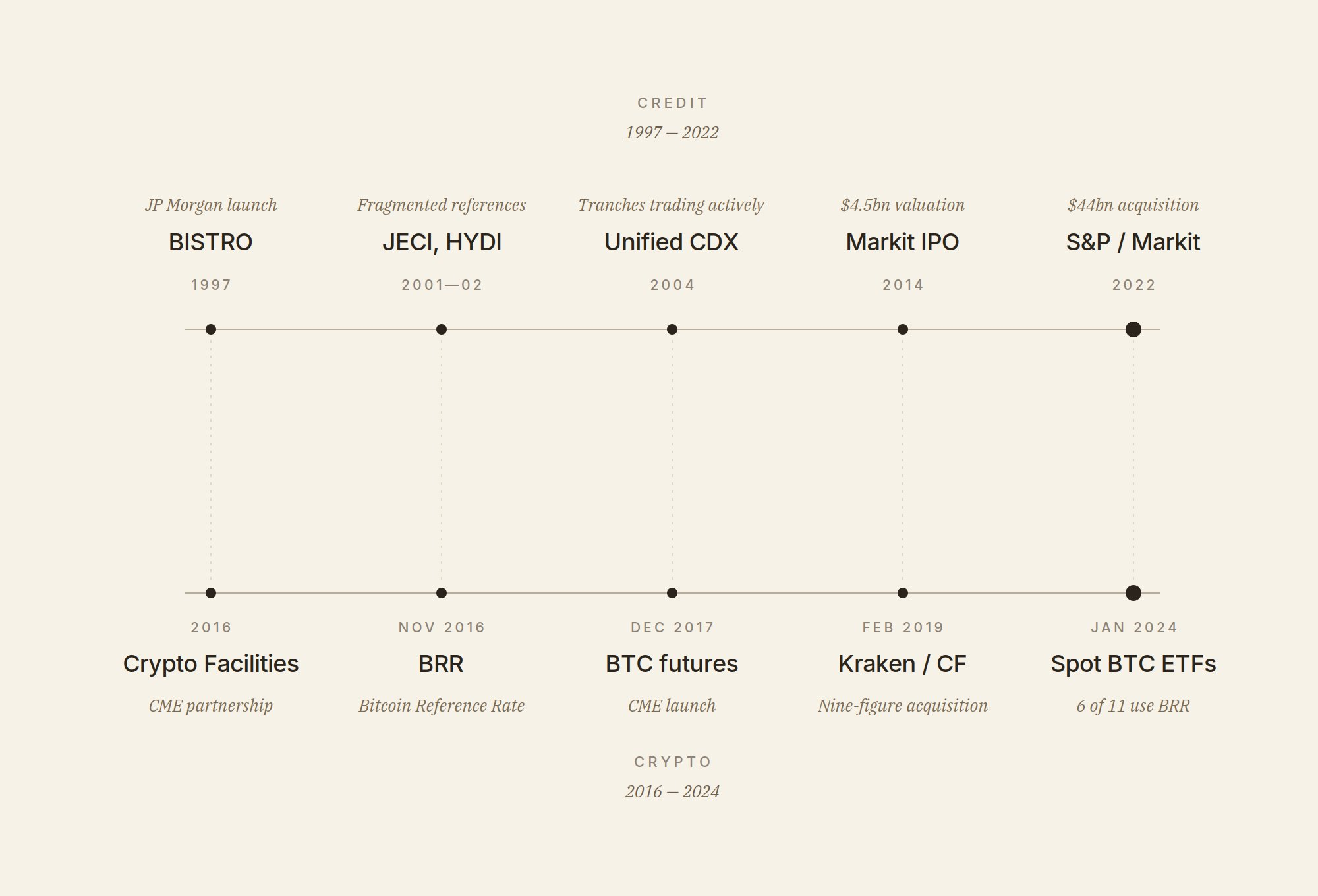

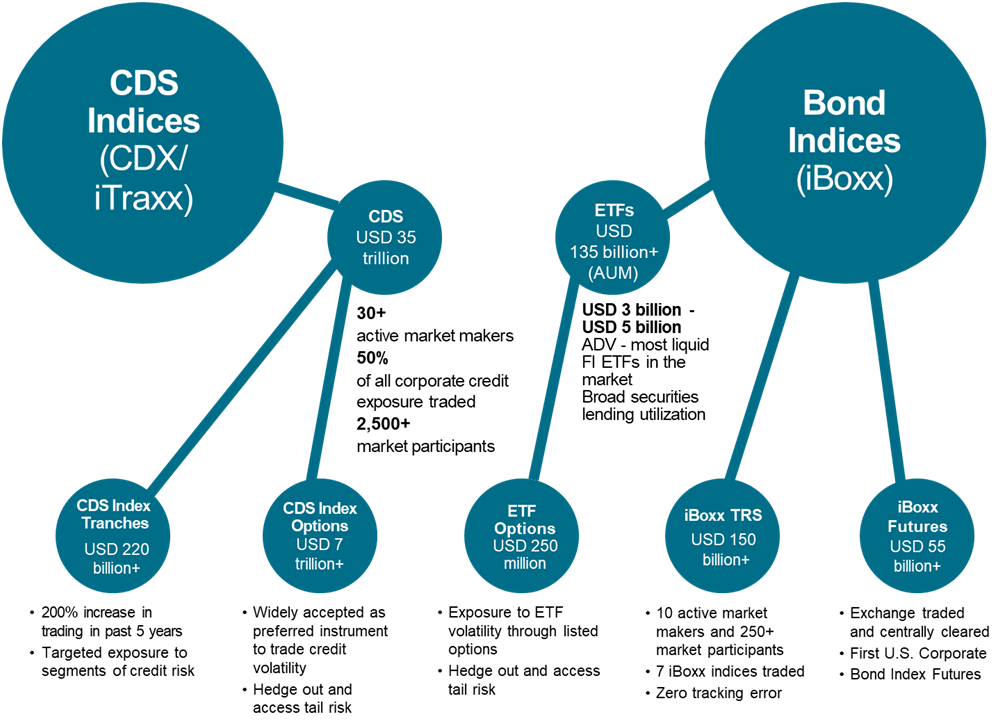

Credit ran this over seven years. JP Morgan's BISTRO standardized synthetic credit risk transfer in 1997. Dealer-consortium indices fragmented in 2001 and 2002 (JECI, HYDI, Synthetic TRACERS), then merged into a unified family in 2004. Tranches were trading actively by mid-2004. Markit consolidated the index IP, IPO'd in 2014 at $4.5bn, and IHS Markit was acquired by S&P Global for $44bn in 2022. The CDS index methodology underneath the structured-credit franchise was a core valuation driver in both transactions.

Crypto ran it over eight. CME and Crypto Facilities partnered in 2016. The Bitcoin Reference Rate published in November of that year. Bitcoin futures came online in December 2017. When the SEC approved spot Bitcoin ETFs in January 2024, six of the eleven approved products chose BRR for their NAV calculation. CF Benchmarks, which was founded with under five people and roughly $1.5m in outside funding, was acquired by Kraken for nine figures. A licensing-only methodology shop, with no balance sheet of its own and no proprietary venue, captured value disproportionate to its operational footprint, because the asset class needed the layer and the layer was scarce.

Markit and CF Benchmarks captured what they captured because once a wrapper settles against a reference, switching costs accumulate fast. New ETFs file against existing benchmarks, new structured products settle against established methodologies, and the first benchmark family that earns institutional adoption becomes the reference for the next decade of products. Disrupting an entrenched reference rate is structurally hard for the same reason that disrupting Treasury auction conventions is hard.

So multiple teams converging on the same target makes structural sense. The institutional stack arriving above is real and deepening, the layer beneath it is empty, and whoever fills it correctly captures what Markit and CF Benchmarks captured. The arithmetic for that has been done out twice already in the past two cycles.

The cost test

A benchmark is useful if and only if the contracts it indexes are structurally cheaper to hedge against than whatever institutional desks are already using to hedge the same risk. If they're not, the wrappers above the benchmark price worse than the alternatives, allocators look at the wrapper and decide they'd rather keep doing what they're already doing, and the benchmark sits there pulling no AUM. The methodology can be flawless. What determines whether the index gets used is whether the underlying contracts pass the cost test.

A few months ago I created an analytical framework to understand this regime shift and what might actual work for institutional risk-transfer using prediction markets. You can check it out in more depth at www.slampaper.xyz if you want to learn more, but I will do my best to summarize my thesis on some of the core components here.

The first is whether a deliverable alternative exists. If institutions can take exposure to the underlying directly through spot, futures, or listed options, then the existing infrastructure already does the price discovery and risk transfer. Event contracts on those categories are competing against decades of mature liquidity, and prediction markets don't have anything to add. The categories where prediction markets do have something to add are the ones where the underlying isn't directly tradeable on existing markets, or you're using N-hop proxies.

The second axis is the size of the variance risk premium in whatever replication alternative does exist. This is the load-bearing measurement, and the rest of this section is about why.

Variance risk premium (VRP) is the spread between the volatility the options market prices at the time of the trade and the volatility that actually realizes over the life of the position. Implied minus realized. It's the difference between what the vol-seller charges and what they end up paying out. Across most categories with a deep options market, since the literature began documenting it in the early 2000s, the spread is persistently positive. Implied runs above realized. Carr and Wu document it across equities; Bollerslev, Tauchen and Zhou document it for the S&P.

VRP is fair compensation. The vol-seller earns the premium because they bear real risks the buyer doesn't carry: jump risk (the seller is exposed to the next jump, which the buyer's realized window didn't include), model uncertainty (no model captures all of the volatility dynamics), and regime shifts (the parameters that governed yesterday's realized aren't necessarily tomorrow's). The premium compensates the seller for that exposure.

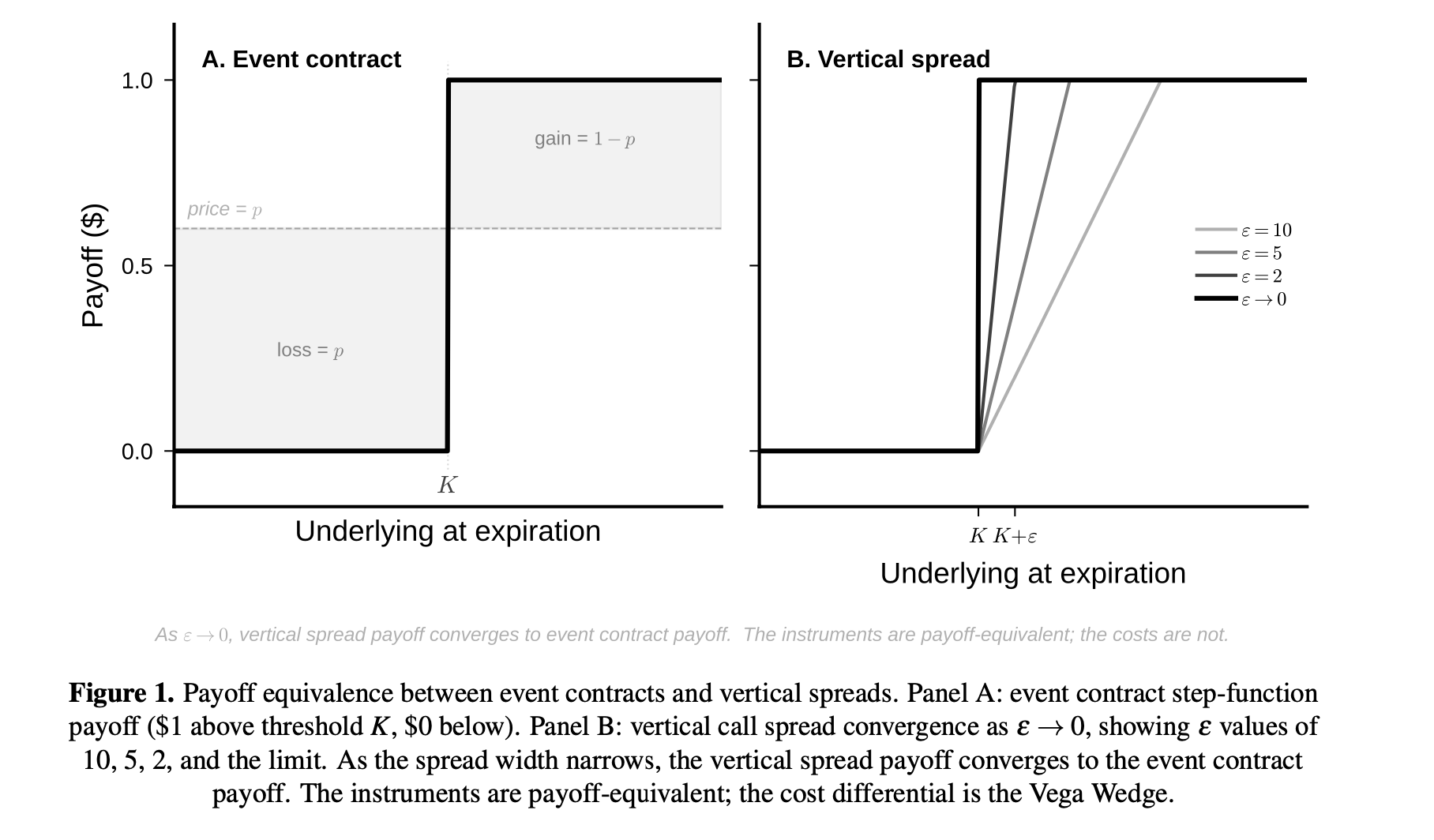

The piece that matters for prediction markets is what VRP is the price of. Options bundle two things: state coverage and path coverage. The hedger using options replication to cover a binary event wants state coverage. Take the Marex investor on the Nvidia-stays-largest note: what they want is protection on the terminal state, did Nvidia stay largest at resolution or didn't it. The options market doesn't sell state coverage separately. It sells the bundle, and the hedger pays VRP on top of the state component because the bundle includes path coverage they don't actually want.

Event contracts are the unbundled version. They price the terminal state, period. When an institution covers a binary event with an event contract instead of an options replication, the path-coverage premium disappears, and the savings is exactly the VRP component of the wedge. That's why VRP is the right tool. It's the academically-quantified price of the bundling problem that event contracts structurally avoid. The mechanism and the measurement are the same thing seen from two sides.

The other two components of the wedge add to this at the margins. Dealer balance sheet cost: options replication consumes dealer capital (inventory carry, gamma management, regulatory capital charges) and the dealer recovers the cost in the spread it charges the wrapper. Event-contract hedging is collateralized at the venue and doesn't run through the dealer's book the same way. Replication friction: the basket of options that approximates a binary payoff carries path-dependency the binary doesn't, and the dealer charges spread to manage the resulting basis.

The 2×2

Two axes, four cells. Each cell behaves differently because the rent dynamics are different.

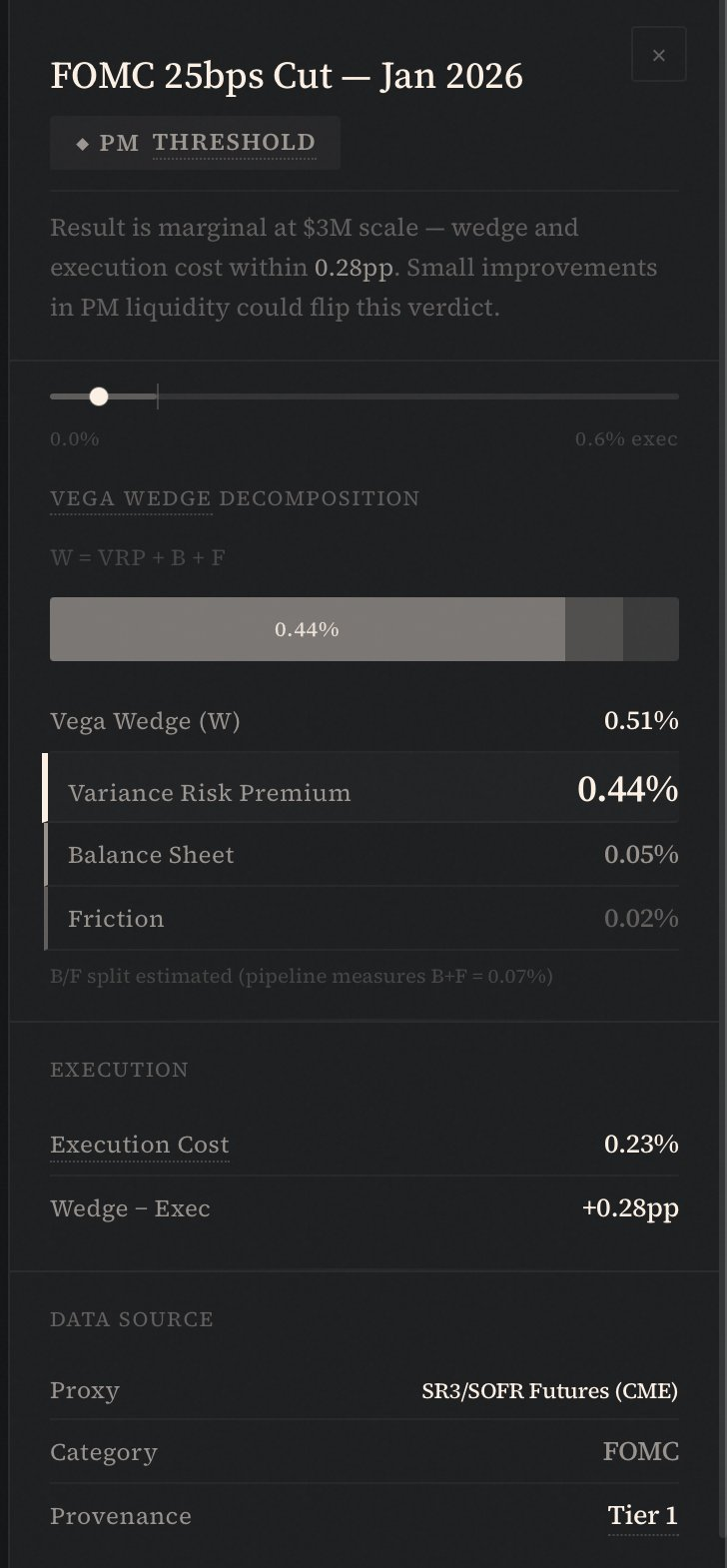

Deliverable, high VRP. The underlying is tradeable, but the listed options market prices the path-coverage bundle expensively. Prediction markets win this cell when PM execution cost at institutional reference size is below the wedge. The cost test is currently being passed in this cell.

Deliverable, low VRP. The underlying is tradeable AND the path-coverage premium has been competed away. FOMC is the cleanest example. SR3 options are deep, dealers compete on the spread, the policy path is telegraphed, and VRP gets compressed to ~50 basis points.

Non-deliverable, high VRP. No tradeable underlying, and even the closest proxy hedges carry expensive bundling. Elections sit here cleanly. There's no spot for "Republicans win the House." The closest replication is country-ETF options, which carry significant VRP, basis risk, and political-cycle skew layered on top. The category is structurally non-deliverable, and the rent is maximal because no arbitrage mechanism exists that could collapse it. Prediction markets win this cell by default; the only question is PM venue depth at institutional reference size.

Non-deliverable, low VRP. Mostly vacuous as a category. If there's no tradeable underlying and no expensive replication alternative, the question to ask is whether anyone actually has an institutional hedging need. Most general-sentiment markets and low-stakes resolution contracts land here.

What VRP varies with

Two pressures explain why VRP varies across categories, and the variation is what produces the temporal sequence of which benchmarks come online when.

Central bank communication compresses VRP at the low end. FOMC, CPI, ECB, equity index resolutions tied to scheduled macro prints. The policy path is telegraphed in advance, the derivatives are deep, plenty of participants compete to sell vol, and the premium gets arbitraged down to whatever's left at measurement time, which isn't much. The compression is structural: the more transparent the policy regime, the narrower the wedge in the deliverable replication. These categories sit in the deliverable + low VRP cell whether or not the PM venues mature, because the bundle isn't expensive to begin with.

The temporal ordering follows. High-VRP categories cross the cost test first because the wedge is wide enough to absorb meaningful execution friction at institutional position size, and they cross as soon as PM depth scales.

Non-deliverable + high VRP categories cross by default once depth exists, because there's no listed alternative competing for the flow. Deliverable + high VRP categories cross when PM execution cost falls below the wedge.

What's being built

One thing before running the framework. Margin engines are a parallel build-out producing the same wave: you can't trade event contracts on institutional margin without them, and the absence of a margin layer gates institutional flow as much as the absence of a benchmark layer does. I'm not addressing margin in this piece because the cost test is the methodology question, but the dual nature of the build matters and the omission is worth flagging.

First, elections.

Roundhill first. Six prediction-market ETFs listing Monday: 2026 Senate, 2026 House, 2028 Presidential, each as Republican and Democratic outcome funds. Bitwise and GraniteShares filed parallel slates against the same logic. Election markets at major maturities sit cleanly in the non-deliverable + high VRP cell. There's no spot for "Republicans hold the House," and the closest replication (country-ETF options on the proxy equity) carries both VRP and significant basis risk against the binary outcome. SLAM measured 12 of 17 election event-periods as PM-wins on cost, with the median wedge running near 0.48 of baseline implied volatility on country-ETF proxies, meaning the savings from hedging an election outcome with PMs rather than ETF options replication is roughly half of the entire ATM IV on the proxy. That's a wide wedge, and PM depth on the major-cycle markets is substantial and growing into listing date.

The methodology question is how the index handles contract-level variation within a category. Roundhill is shipping six funds across three races, and each race resolves through a slate of contracts (margins of victory, congressional seat counts, presidential state-by-state) with very different depth distributions across the slate. A naive methodology that selects all contracts in an event-period as eligible constituents will include constituents below institutional reference size alongside the ones that clear it, and any wrapper marking against the index inherits the pricing of the below-threshold constituents every time it rebalances through them. Equity indices don't run into this because float-adjusted market cap automatically gives you the deep names. PM benchmarks need a contract-level depth filter, because the depth distribution within a PM category is much wider than within an equity universe, and the methodology that ships first into election ETFs and gets the contract-level filter right captures the reference position for the entire category.

Secondly, corporate events.

Marex's CLN sits in the same cell on a different underlying type. Nvidia-stays-largest is a corporate-event contract on a name with a very deep equity options market, so the closest replication is structurally expensive: a basket of single-name options on the top mega-cap contenders, rebalanced as caps move, picking up VRP on every leg, with the basis between the basket's terminal payoff and the binary outcome adding compounding ugliness. The Kalshi/Polymarket leg is structurally cheaper, and the spread between Marex's 7% coupon and its hedge cost is the wedge being captured. The structure is repeatable. A benchmark on corporate-event contracts of this kind (largest-by-cap rotations, leadership tenure, M&A outcomes on names with deep options surfaces) would let twenty other structurers price the Marex-style trade against a published reference rather than a bilateral mark.

Thirdly, the currently missing cluster of KPIs and AI

Where the indices race should be running, instead, is the densest cluster of non-deliverable + high VRP contracts currently sitting on Kalshi and Polymarket without a benchmark layer above them. That cluster is AI capability markets and company KPI markets, by a meaningful margin. Kalshi runs monthly and weekly best-AI-model markets resolving against the LM Arena leaderboard, with both model-level and company-level variants, plus capability-threshold contracts on Arena scores and named model-release dates.

The KPI side spans Tesla quarterly deliveries (KXTESLA), earnings outcomes for major tech names, and a growing roster of company-performance markets across the mega-caps. None of these have a tradeable underlying. The closest replication for "Anthropic ranks first on Arena at month-end" is a basket of single-name equity options on AI-exposed names, which is structurally orthogonal to model leaderboard ranking and carries single-name VRP that runs higher than index VRP across most measurement windows. Earnings options are the textbook-expensive vol surface in the equity universe, which is why the IV crush around earnings is one of the most-documented patterns in derivatives data.

The methodology shop that ships first into this cluster captures the reference position for an exposure category that didn't have institutional pricing infrastructure before PM venues built it. AI capability and company KPI are not categories institutional desks have a clean derivative to hedge through today.

I know the @affaanmustafa and the @ito_markets team are looking into this more deeply. This is what interests me the most in terms of the benchmark design space.

The ordered call

Two tiers. Top tier is where the indices race should be running, sorted by current build state. Bottom tier is everything outside the thesis, handled briefly.

Top tier

Election markets at major maturities are crossed today on cost and being shipped against. Roundhill, Bitwise, and GraniteShares are all building methodology slates, and the first credible family with contract-level depth filtering captures the reference position.

Corporate-event contracts on names with deep equity-options proxies are crossed on the contracts where PM depth has scaled. One structurer (Marex) has priced one note. The rest of the desk universe is waiting on a benchmark to do the trade in series.

AI capability and company KPI markets are the densest cluster of contracts in the cell with no benchmark layer above them.

Geopolitical resolution contracts are similar in shape and depth-gated. Major election cycles qualify across the board.

Bottom tier

Macro print contracts (CPI, FOMC, ECB, BOJ, GDP) sit in deliverable + low VRP and don't cross. The bundle is competitively priced in Treasury and rates options because the policy regime is transparent and the derivative is deep.

Closing

There's a structural wrinkle here that's specific to this asset class, and it's the reason running the cost test upstream isn't optional. In credit and crypto, the test got answered implicitly. By the time the BRR published in November 2016, Bitcoin spot markets had spent years clearing exchange-quality, concentration, and arbitrage-bandwidth thresholds; the wrappers came after the implicit test had been passed.

The CDX comp ran the same way over a longer arc. In both cases, the underlying was deliverable, which means there was a spot market that could mature, which means the cost test could be run by the market itself on a timescale of years before any benchmark shipped. The benchmark codified what the maturation produced.

The cell the indices race is shipping into now doesn't have that. Non-deliverable + high VRP underlying has no spot to mature. Elections, AI capability outcomes, and company KPI prints all share the same property: no spot to arbitrage, no derivatives surface to compress vol on, no implicit test running in the background.

The cost test can't be answered through years of maturation in the underlying because there is no underlying to mature. So either the methodology shop runs the explicit test upstream, by measuring VRP in the closest replication and locating the underlying contracts in a cell where the cost test can be passed, or the test gets run downstream by allocators looking at wrapper performance after the fact.

However, the companies who do this successfuly will have built, based on historical precedent, some of the highest margin businesses in finance for a novel asset class.